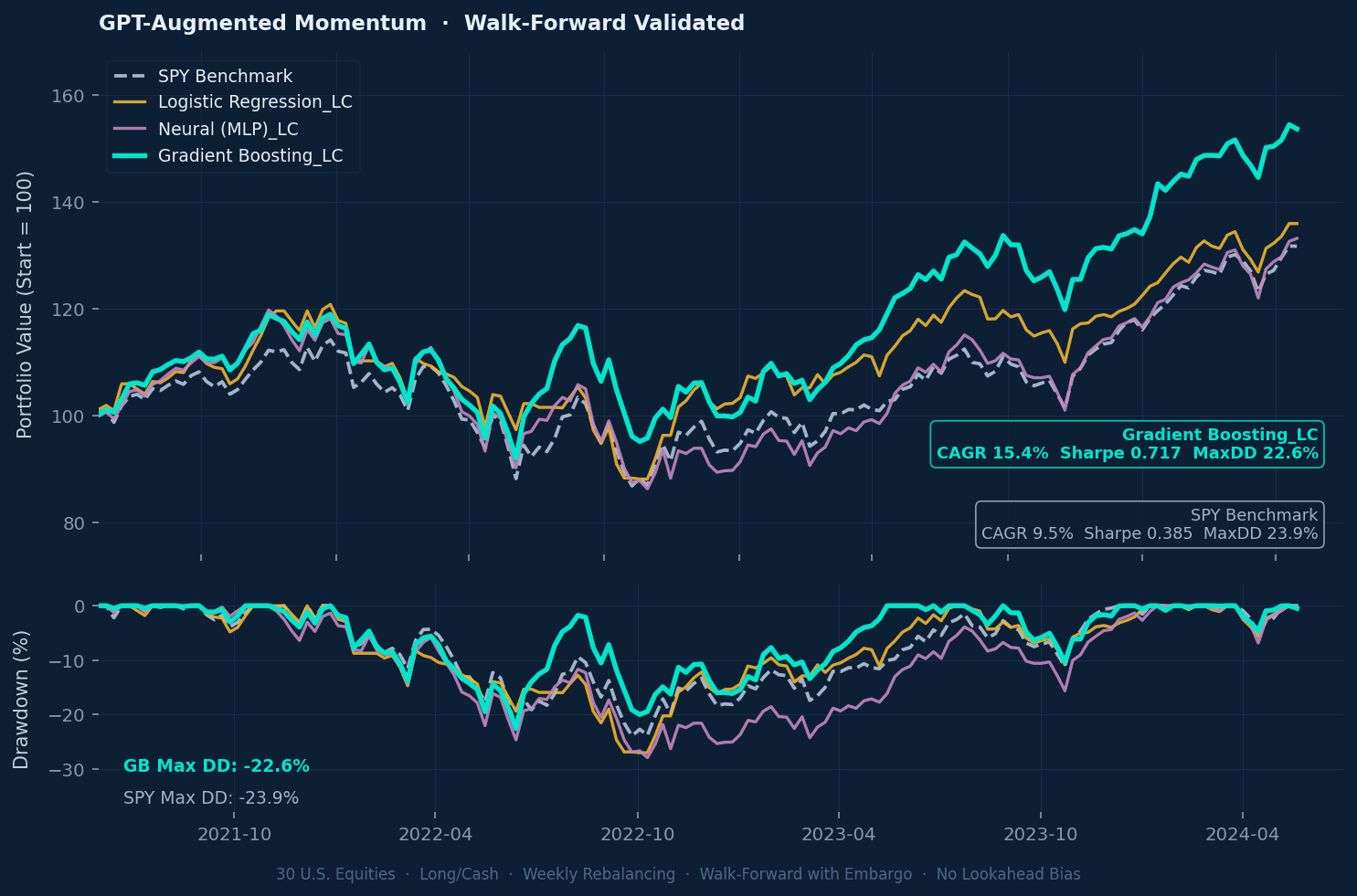

15.4%CAGR

0.717Sharpe Ratio

22.6%Max Drawdown

5 yrsOut-of-Sample

The one metric that separated

real alpha from overfitting

A free research kit for quant researchers, PMs, and algo traders — equity curves, methodology, and a Python notebook you can run in Google Colab in 5 minutes.

Strategy Results PDF

Methodology One-Pager

Python Colab Notebook

Early Access — Issue 02

Get the Research Kit — free

Enter your name and email. No credit card. No account creation.

No spam. Unsubscribe anytime. New issues published monthly.

The Signal · Issue 01 · April 2026

Walk-Forward Validated · 2019–2024

Strategy Performance vs Benchmark

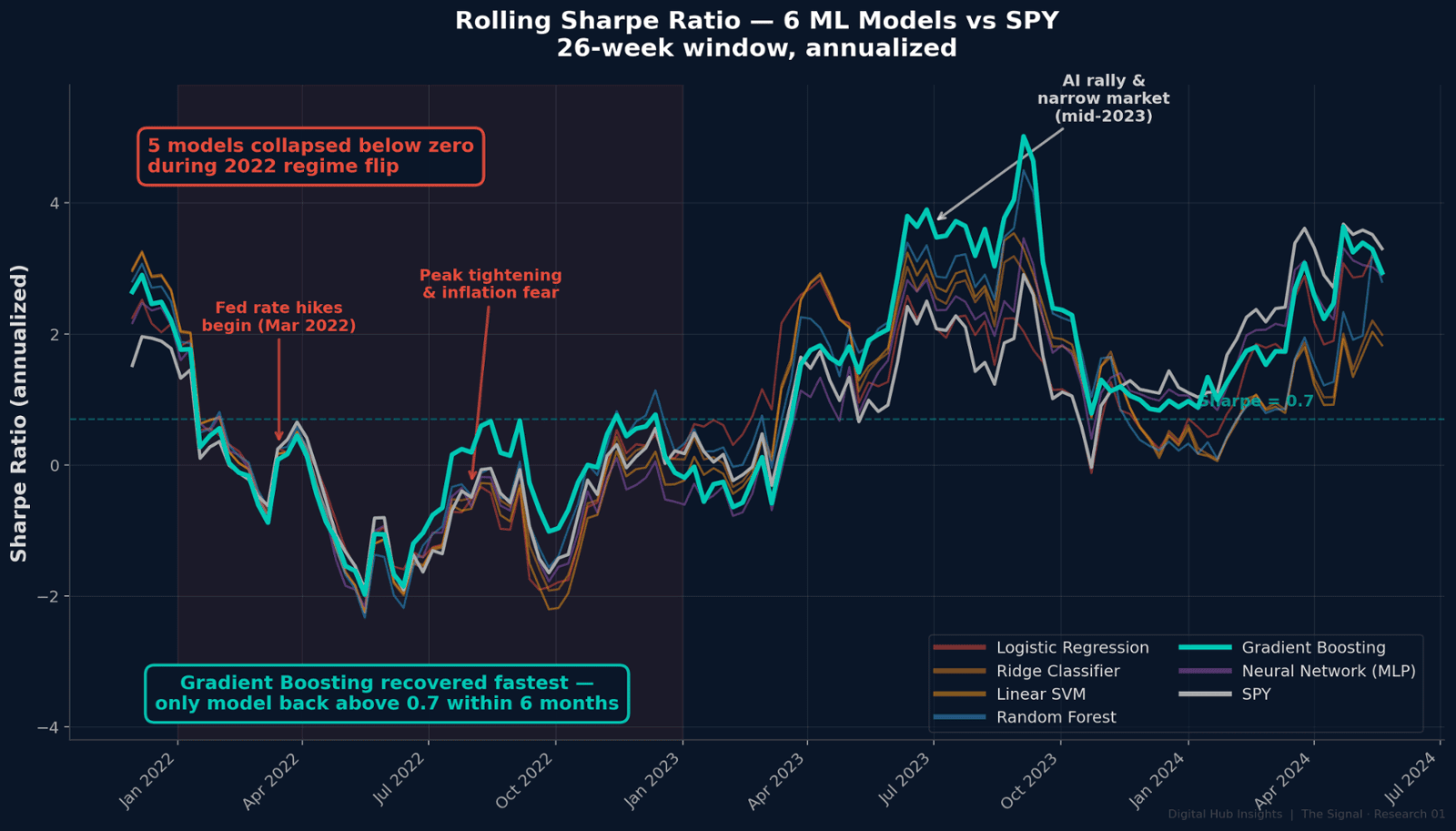

Risk-Adjusted Performance Through Market Regimes

Rolling Sharpe Ratio — How Models Survived 2022

Static Sharpe ratios hide the real story. This 26-week rolling window reveals which models collapsed during the 2022 rate shock — and which recovered fastest. Gradient Boosting was the only model back above 0.7 within six months.

26-week rolling window · Annualized (√52) · Walk-forward validated 2019–2024

Canonical Results

By the Numbers

| Model | CAGR | Sharpe | Max DD | Final Value |

|---|---|---|---|---|

| Gradient Boosting | 15.4% | 0.717 | −22.6% | $166K |

| XGBoost | 14.1% | 0.691 | −21.8% | $159K |

| Random Forest | 12.7% | 0.654 | −24.1% | $148K |

| SPY Benchmark | 9.5% | 0.385 | −23.9% | $133K |

"GPT-augmented pipelines now compress months of research into hours. But humans retain control of credibility — data integrity, leakage detection, economic plausibility. The bottleneck in quant research has shifted from implementation to judgment."

Mehrzad Mahdavi, PhD · Founder, Digital Hub Insights

Former CIO · 30+ years in data science & algorithm development

Get the Research Kit. Free.

Two PDFs + walk-forward code template. Real data. Walk-forward validated.

Get the Research Kit →